Explore different types of health insurance plans in India, including individual, family floater, critical illness, and top-up options for comprehensive coverage.

Types of health insurance plans in India and how to choose

Health insurance in India is not a one-size-fits-all product. Different life stages, family structures, and health conditions call for different types of health insurance plans. If an individual plan suits a single person with specific health risks, a family floater might be better for young families seeking cost-effective coverage. Likewise, a critical illness policy provides a lump sum for life-threatening diagnoses. Therefore, understanding the types of health insurance and how they apply may help you make an informed decision.

What is health insurance?

Health insurance is a contract between you and an insurance company in which you pay a regular premium in exchange for coverage of medical expenses. The insurer pays for or reimburses covered medical expenses, such as hospitalisation, surgery, diagnostics, pre and post-hospitalisation expenses, and day-care procedures (treatments that do not require 24-hour hospitalisation, such as cataract surgery or chemotherapy), as per the policy terms. Without health insurance, a single hospital admission for a serious condition can cost several lakh rupees, depleting savings or pushing families into debt. Health insurance transfers this financial risk to the insurer, making quality healthcare accessible without catastrophic out-of-pocket spending.

Read more information about Health Insurance: Complete Overview of What, Why, How & Coverage

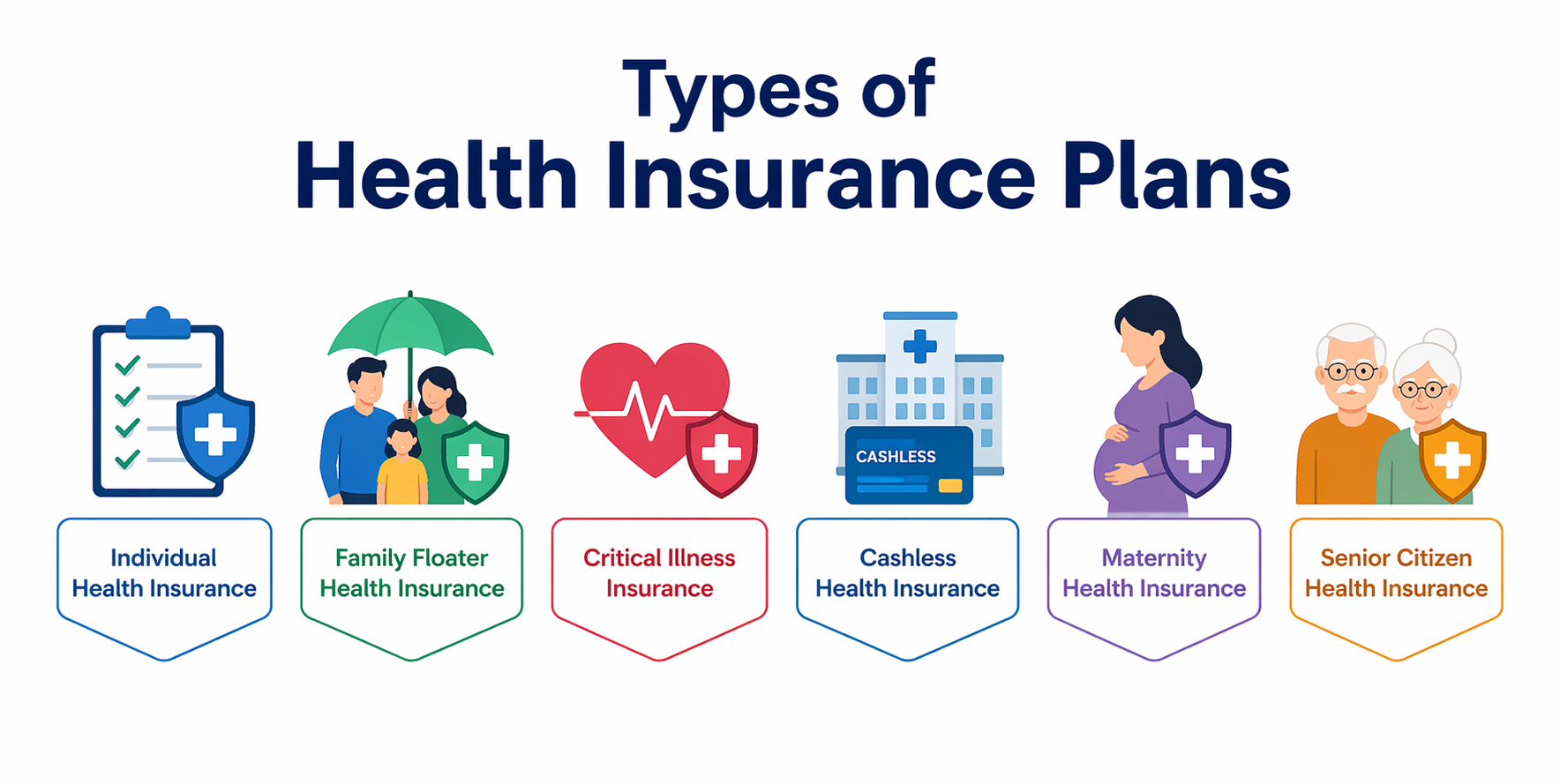

Types of health insurance plans in India

The health insurance market in India offers a wide range of plan categories, each designed to address different life stages, financial situations, and healthcare needs. Understanding these options can help you choose coverage that aligns with your personal requirements and long-term financial security.

1. Individual health insurance

An individual health insurance plan covers a single person under one policy with a dedicated sum insured. The entire coverage amount is available exclusively for that person's medical expenses. This type of plan is ideal for working professionals, individuals with pre-existing conditions who need personalised coverage, and people who want a sum insured that is not shared with family members. The premium is calculated based on the individual's age, health history, and chosen sum insured.

2. Family floater health insurance

A family floater plan covers multiple family members under a single policy with a shared sum insured. Typically, it includes the policyholder, spouse, and dependent children, with some plans also covering parents. Any insured member can use the sum insured during the policy year. Family floater plans are more affordable than buying separate individual policies for each member because the premium is based on the age of the eldest member. However, since the sum insured is shared, a major claim by one member reduces the coverage available for others during the same year.

3. Senior citizen health insurance

Senior citizen plans are designed for individuals aged 60 and above. These plans account for the greater medical needs of older adults and typically cover age-related conditions. Pre-existing diseases are typically covered after a waiting period of 2 to 4 years, depending on the insurer and policy terms. Premiums are higher than standard individual plans due to the increased health risk associated with age. Some insurers offer plans with entry ages as high as 75 or 80 years and lifelong renewability, ensuring continuous coverage throughout the policyholder's life.

4. Critical illness insurance

A critical illness policy pays a lump-sum amount upon diagnosis of a specified critical illness, regardless of the actual treatment costs. Common conditions covered include heart attack, stroke, cancer, kidney failure, organ transplant, and major burns. The payout is a single lump sum that the policyholder can use for treatment, recovery, lifestyle adjustments, or income replacement during the period when they are unable to work. Critical illness plans complement regular health insurance rather than replacing it, providing an additional financial cushion for life-threatening diagnoses.

5. Group health insurance

Employers provide group health insurance to their employees and sometimes their dependents as part of the company's benefits package. The employer pays the premium (in full or in part), and all eligible employees are covered under a single master policy. Group plans offer standardised coverage, usually without medical underwriting, which means employees with pre-existing conditions are covered from day one. However, group coverage ends when the employee leaves the organisation, making it important to have a personal health insurance plan as backup.

6. Top-up and super top-up plans

Top-up plans provide additional coverage above a specified threshold called the deductible. The deductible is the amount you pay out of pocket (or through your base policy) before the top-up plan starts covering expenses. For example, if your base plan has a sum insured of ₹5 lakh and you buy a super top-up with a ₹5 lakh deductible, the top-up covers expenses exceeding ₹5 lakh per year. Super top-ups are cost-effective ways to significantly increase your total health coverage without paying the high premiums of a standalone plan with a very large sum insured.

7. Personal accident insurance

Personal accident insurance provides compensation for accidental death, permanent total disability, permanent partial disability, and temporary total disability resulting from an accident. Unlike health insurance, which covers illness and hospitalisation, personal accident insurance specifically addresses accidents and their financial consequences. It pays a lump sum or weekly benefit based on the severity of the injury or disability. This type of cover is relevant for individuals with high-risk occupations, frequent travellers, and anyone who wants financial protection specifically against accident-related outcomes.

8. Disease-specific health insurance

Some insurers offer policies that cover specific diseases or conditions, such as diabetes management plans, cancer care policies, or cardiac care plans. These policies provide targeted coverage for the diagnosis, treatment, and ongoing management of a specific condition. They are useful as supplementary coverage for individuals who are at higher risk of a particular disease due to family history or existing health indicators.

Comparison of types of health insurance plans

The table below provides a quick comparison of different types of health insurance plans based on their suitability, coverage structure, and key features.

Plan Type | Best For | Sum Insured | Key Feature |

Individual | Single person, personalised needs. | Dedicated to one person. | Tailored coverage based on individual risk. |

Family floater | Young families, couples with children. | Shared among all members. | Cost-effective with a single premium. |

Senior citizen | Parents aged 60+. | Dedicated, higher premiums. | Covers age-related conditions. |

Critical illness | High-risk individuals, income earners. | Lump sum payout on diagnosis. | Covers specific life-threatening diseases. |

Group | Employees of an organisation. | Standardised for all employees. | No medical underwriting, employer-paid. |

Top-up / Super top-up | Those with existing base coverage. | Covers expenses above deductible. | Affordable way to increase coverage. |

Personal accident | Frequent travellers, high-risk jobs. | Lump sum for accident outcomes. | Covers accidental death and disability. |

Disease-specific | High-risk for specific conditions. | Targeted for one disease. | Supplementary coverage for specific risks. |

This comparison helps you understand how each plan differs, making it easier to identify the options that align with your specific needs and coverage priorities.

How to choose the right type of health insurance plan?

Selecting the right plan requires evaluating your personal and family circumstances against the features of each plan type.

Assess your current life stage: A young, single professional may need an individual plan. A married couple with children benefits from a family floater. Parents above 60 need a senior citizen plan.

Evaluate your health risks: If you have a family history of heart disease or cancer, adding a critical illness plan provides an extra layer of protection beyond your regular health coverage.

Determine the right sum insured: Factor in medical inflation (10% to 15% per year in India), the cost of hospitalisation in your city, and the number of family members covered. A sum insured of around ₹10 lakh or higher is commonly recommended for families in metro cities.

Check waiting periods: Most health insurance plans also have an initial waiting period of around 30 days, except for accident-related claims. Review policy exclusions carefully, as certain conditions, treatments, or diseases may not be covered.

Review the network hospital list: Ensure that hospitals near your home and workplace are part of the insurer's cashless network for convenient claim processing.

Compare claim settlement ratios: A higher CSR indicates the insurer settles a larger percentage of claims, reflecting better reliability.

Choose a reliable insurer: Zurich Kotak General Insurance offers multiple health plans, including individual, family floater, senior citizen, and top-up options.

Consider add-ons and riders: Maternity cover can also be added to some plans to cover pregnancy and childbirth-related expenses.

Use top-ups to boost coverage affordably: If your base plan has a sum insured of ₹5 lakh, a super top-up with a ₹5 lakh deductible and ₹20 lakh coverage gives you ₹25 lakh total coverage at a fraction of the cost of a standalone ₹25 lakh plan.

Tax benefits of health insurance under Section 80D

Premiums paid for health insurance qualify for tax deductions under Section 80D of the Income Tax Act.

Self and family (aged below 60 years): Deduction of up to ₹25,000 per year.

Parents (below 60 years): Additional deduction up to ₹25,000 per year.

Parents (60 years and above): Additional deduction up to ₹50,000 per year.

Preventive health check-up: Expenses up to ₹5,000 are included within the overall Section 80D limit.

This means a family with senior-citizen parents can claim up to ₹75,000–₹1,00,000 in total deductions, depending on eligibility, thereby reducing the effective cost of premiums.

Conclusion

The types of health insurance available in India include individual plans, family floater plans, senior-citizen plans, critical-illness policies, group insurance, top-ups, personal accident covers, and disease-specific plans. Each serves a different need, and most families benefit from a combination of two or more plan types for comprehensive coverage. The right health insurance plan depends on your individual needs, financial situation, and health risks.

Read more - OPD vs IPD – Difference Between OPD and IPD

FAQs

Q1: What are the main types of health insurance in India?

Individual, family floater, senior citizen, critical illness, group, top-up, personal accident, and disease-specific plans are the main types.

Q2: Which type of health insurance is best for families?

A family floater plan is cost-effective for young families. Adding a super top-up increases coverage affordably for the entire family.

Q3: Is critical illness insurance the same as health insurance?

No, critical illness pays a lump sum on diagnosis. Health insurance covers hospitalisation and treatment costs. Both complement each other.

Q4: What is a super top-up health insurance plan?

A plan that covers medical expenses exceeding a specified deductible amount, providing additional coverage above your base health insurance policy.

Q5: Should I buy health insurance if my employer provides group coverage?

Yes, group coverage ends when you leave the job. A personal plan ensures continuous coverage regardless of employment status.

Q6: What tax benefits are available for health insurance premiums?

Deductions under Section 80D: up to ₹25,000 for self and family, plus up to ₹50,000 for senior citizen parents per year.

Q7: How much sum insured should I choose?

At least ₹10 lakh for families in metro cities. Consider medical inflation and the costs of major procedures when setting the coverage amount.

Q8: Can I have multiple types of health insurance plans?

Yes, combining a base plan with top-up, critical illness, and personal accident plans provides comprehensive, multi-layered coverage.

Explore more on health insurance

Easy access to more, check out these quick links

Get Quick Quote