Read about Consequences of not having a health insurance plan. For more information, check out the health insurance plans from Zurich Kotak General Insurance.

Consequences of being without health insurance in India

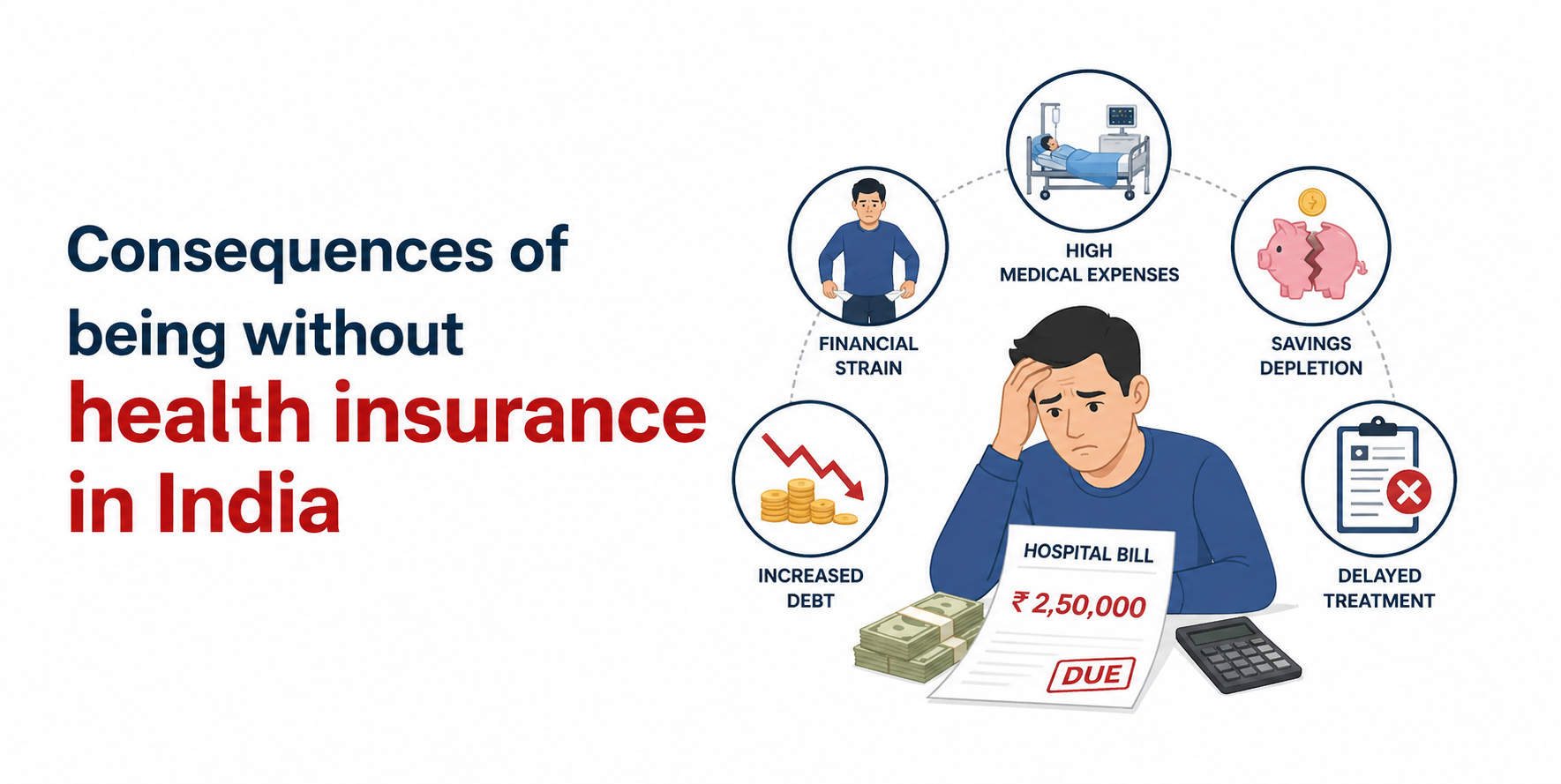

While there is no legal requirement to buy health insurance in India, remaining uninsured exposes you to severe financial and medical risks. In a country where healthcare costs are rising rapidly, and a large share of spending remains out‑of‑pocket, a single hospital stay can wipe out substantial savings or push families into long‑term debt. Being left with no health insurance means you must bear the full weight of expensive surgeries and treatments yourself, often leading to long-term debt and immense stress for your family. Understanding these serious risks is a vital step in ensuring that a sudden medical crisis does not compromise your long-term financial stability or your ability to afford quality care when it matters most.

1. No legal penalty but high financial risk

Unlike in some countries, there is no nationwide legal penalty or fine for not having private health insurance in India. However, without cover, you must pay all medical bills yourself, which can be financially devastating if a major illness or hospitalisation occurs.

2. High and unpredictable medical expenses

Medical emergencies like accidents or critical illnesses often result in massive hospital bills, sometimes reaching lakhs or even crores of rupees. If you have no health insurance, you have to pay these costs using your own cash, which can quickly drain your bank accounts.

Health insurance plans typically cover:

Costs for hospital stays, including room rent and ICU charges.

Medical expenses incurred both before admission and after discharge, usually for a period of 30 to 60 days.

Advanced treatments or surgeries that do not require a full 24-hour hospital stay.

Charges for emergency transport to the hospital via ambulance.

Medical care is provided at home if the patient cannot be moved or if hospital beds are unavailable.

Costs related to the surgical harvesting of organs from a donor.

Expenses for pregnancy, delivery, and infant care, depending on the specific plan.

Professional treatment for psychiatric or mental health conditions in line with official regulations.

3. Risk of falling into debt

If you are without medical insurance, you may be forced to borrow money from friends or take high-interest loans to cover hospital charges. This creates a cycle of debt that can ruin your family’s financial peace and make it hard to pay for everyday needs.

4. Loss of savings and assets

A single health crisis can swallow years of hard work, emptying retirement funds or forcing you to sell your car or home. A good health policy keeps your wealth safe, so you don't have to sell what you own just to get well.

5. Limited access to quality healthcare

Without a policy, you might hesitate to go to a good hospital or delay treatment because you are worried about the price. This can make a health problem much worse. Having insurance gives you the freedom to choose the best doctors and get treated immediately without worrying about the bill.

6. Increased mental stress and anxiety

The fear of how to pay for a major surgery causes a lot of worry for the whole family. Having a policy removes this tension, letting you focus on getting better rather than counting how much money is left in your account.

7. Missing out on tax benefits

Under Section 80D of the Income Tax Act, you can claim deductions on premiums paid for health insurance for yourself, your spouse, children, and parents, subject to specified limits. The exact deduction limits depend on age and whether the insured is a senior citizen, and may differ between the old and new tax regimes.

Common reasons people avoid health insurance

Many individuals neglect to buy cover due to:

The belief that insurance is unnecessary for the young or healthy.

A lack of clarity regarding benefits and specific coverage.

The assumption that premiums are too expensive.

Relying solely on employer-provided group insurance, which is often inadequate.

It is essential to look past these myths and recognise that insurance is a foundational investment for everyone, regardless of age.

Why is group health insurance often not enough?

Employer-provided cover is a great perk, but it often comes with low limits that may not protect you against major surgeries or long-term illnesses. One of the biggest risks of relying solely on a group plan is that the coverage usually ends the moment you leave your job or retire. This leaves you vulnerable during career transitions or in your later years when you need medical support the most.

Furthermore, group plans are "one size fits all" and may not cover specific needs like critical illness or maternity, as a personal plan would. Holding an individual or family floater plan ensures you have comprehensive, continuous protection that stays with you regardless of your employment status.

How to choose the right health insurance policy?

Securing health insurance is now a straightforward process. You can compare various policies online and select a plan based on your family size, specific health needs, and monthly budget.

When selecting a plan, consider:

An adequate sum insured to account for rising healthcare costs.

Waiting periods for pre-existing conditions.

The list of network hospitals for cashless treatment.

The claim settlement ratio of the provider.

Useful add-ons like maternity or critical illness cover.

Comparison: Consequences vs benefits

Consequences without health insurance | Benefits of health insurance |

Pay full medical bills yourself | Insurer covers hospitalisation costs |

Risk of losing savings and property | Keeps your savings and legacy safe |

Potential for debt and loans | Avoids money worries and loans |

Delayed or poor healthcare | Access to top care and cashless stays |

No tax benefits | Tax savings under Section 80D |

Increased mental anxiety | Peace of mind for the whole family |

Conclusion

Choosing to remain without health insurance in India can lead to significant financial consequences for your family. While having a policy is a personal choice, the high cost of private medical care means that an unforeseen health issue can quickly lead to financial instability. A comprehensive plan serves as a vital safety net, covering hospital bills and offering tax benefits so you can focus on recovery rather than costs. It is much more practical to pay a regular premium now than to face a massive bill during a crisis. Selecting a plan early ensures your family always has access to the best medical support without any financial delay.

FAQs

Q1: Is health insurance mandatory in India?

Health insurance is not a legal requirement in India, and there are no penalties for not holding a policy. However, maintaining comprehensive coverage is strongly advised to mitigate the substantial costs associated with private medical treatment.

Q2: What happens if I face a medical emergency with no insurance?

You will have to find the money to pay for everything yourself. This often leads to depleting your savings or taking out loans that are hard to repay.

Q3: Can group health insurance from my employer suffice?

Generally, these plans are often basic and might not cover the full cost of a serious illness. It is safer to have your own personal plan as well.

Q4: What tax benefits do I get from health insurance?

Under Section 80D, the money you spend on premiums can be used to lower your taxable income, which helps you save a good amount of money every year.

Q5: How does insurance improve access to healthcare?

It lets you get "cashless" treatment, which means the insurance company pays the hospital directly, so you don't have to pay out of pocket before the doctor starts treatment.

Q6: What should I check before buying a plan?

Check the total coverage amount, how long you have to wait for certain diseases to be covered, and which hospitals near you offer cashless payments.

Get Quick Quote