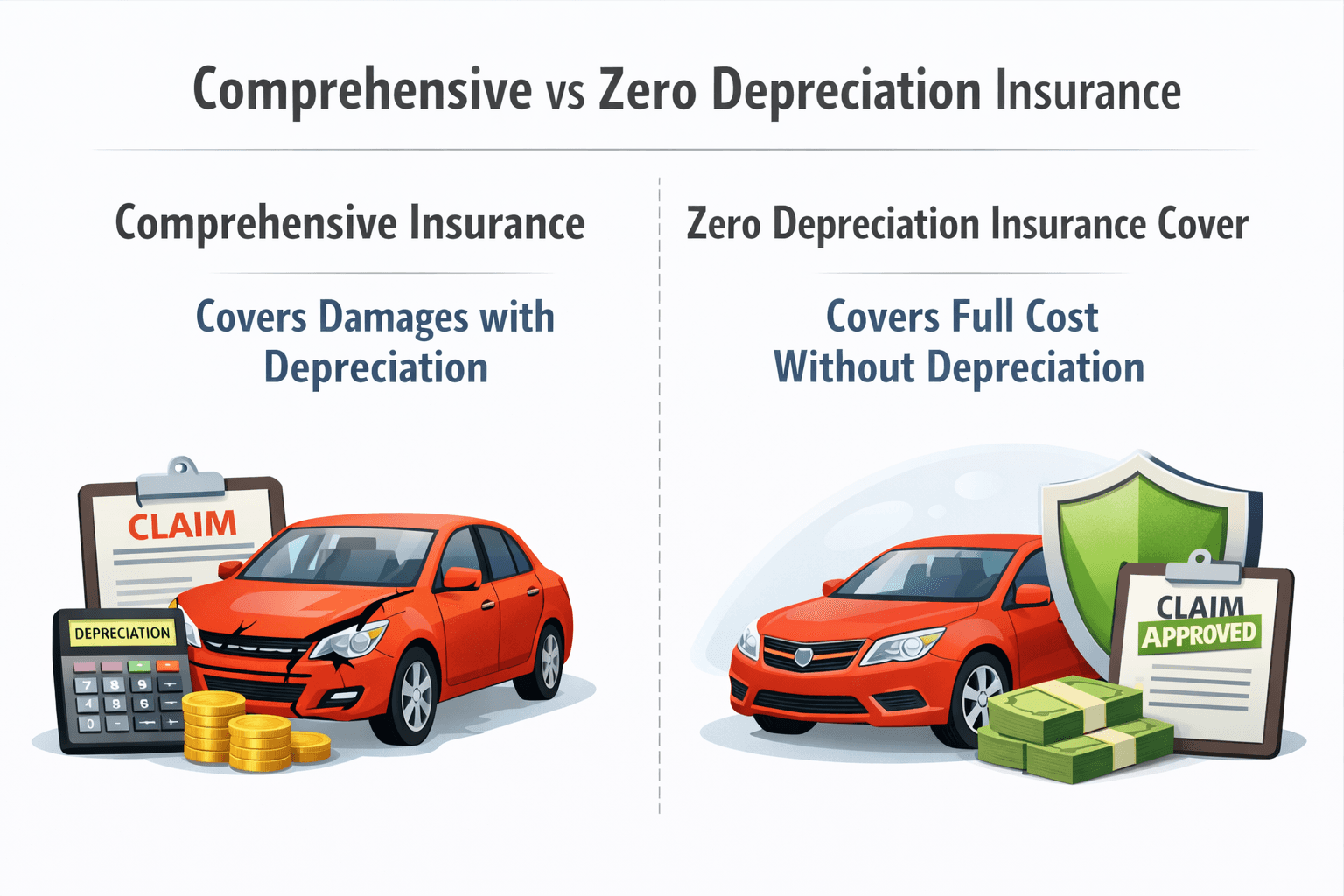

Comprehensive car insurance and zero depreciation cover are related but distinct. Comprehensive insurance is the base policy that covers your vehicle against accidents, theft, fire, natural disasters, and third-party liabilities, but it applies depreciation deductions to replaced parts when you file a claim. Zero depreciation cover is an optional add-on that removes these depreciation deductions, ensuring you receive the full repair cost. Understanding how each works, what they cost, and when to choose one over the other helps you avoid unexpected out-of-pocket expenses during claims.

What is comprehensive car insurance?

Comprehensive car insurance is a motor insurance policy that provides broad coverage for your vehicle. It covers damage from accidents, theft, fire, natural disasters, and vandalism, along with third-party liability for injury or property damage caused to others, and personal accident cover for the insured driver. While it offers extensive protection, the insurer deducts depreciation on replaced parts during claim settlements. This means you bear a portion of the repair cost yourself, proportional to the age and type of the parts being replaced.

How depreciation impacts claims

When you file a claim under comprehensive insurance, the insurer applies depreciation rates to the cost of replaced parts. These rates vary by part type.

Part Type | Depreciation Rate |

Rubber, nylon, plastic parts | 50% |

Tyres, tubes, batteries | 50% |

Fibreglass components | 30% |

Glass parts (windscreen, windows) | Nil (0%) |

Depreciation on Metal Parts (Based on Vehicle Age)

Vehicle Age | Depreciation Rate |

Up to 6 months | 0% |

6 months to 1 year | 5% |

1 to 2 years | 10% |

2 to 3 years | 15% |

3 to 4 years | 25% |

4 to 5 years | 35% |

5 to 10 years | 40% |

Above 10 years | 50% |

What is zero depreciation cover?

Zero depreciation cover , also called bumper-to-bumper insurance , is an optional add-on to your comprehensive policy. It waives the depreciation deduction on replaced parts during claims, so the insurer pays the full repair or replacement cost. This cover is typically available for vehicles up to 5 years old and is especially valuable for new cars, luxury vehicles, and cars driven frequently in high-risk conditions.

Key differences between comprehensive car insurance and zero depreciation cover

Feature | Comprehensive Car Insurance | Zero Depreciation (Add-on) |

Coverage | Own damage, third-party liability, and personal accident. | Same as comprehensive, plus no depreciation deduction on parts. |

Depreciation deduction | Applied to replace parts during claims. | No depreciation deduction on replaced parts. |

Premium cost | Lower premiums. | Higher premiums (typically 15% to 30% more). |

Vehicle eligibility | Available for all vehicle ages. | Usually available for vehicles up to 5 years old. |

Claim limits | No specific claim count limits. | Typically limited to 2 to 3 claims per policy year. |

Out-of-pocket expenses | Higher due to depreciation deductions. | Lower due to full claim settlements. |

Best suited for | Older vehicles, budget-conscious owners. | New vehicles, luxury cars, high-usage drivers. |

Example claim scenario

Suppose your car’s plastic bumper and side mirror need replacement after an accident, costing ₹20,000 in total.

With comprehensive insurance only. Depreciation of 40% on plastic parts means the insurer pays ₹12,000 and you pay ₹8,000 out of pocket.

With a zero depreciation add-on. The insurer pays the full ₹20,000 with no depreciation deduction. Your out-of-pocket cost is zero (excluding any applicable deductibles).

Note: Even with zero dep, the customer may still pay:

Compulsory deductible

Voluntary deductible (if chosen)

Non-covered items (unless add-ons exist)

How zero depreciation affects your premium

Adding zero depreciation cover increases your premium by approximately 15% to 30%, depending on the vehicle age, model, and insurer. For a car with an own-damage premium of ₹15,000, the zero depreciation add-on might cost an additional ₹2,000 to ₹4,500 per year. However, the savings during even a single claim can far exceed this additional cost, especially for cars with expensive body panels and components.

Impact on No Claim Bonus (NCB)

Claims made under zero depreciation cover affect your NCB in the same way as regular comprehensive claims. Filing a claim resets your NCB to zero at the next renewal, regardless of whether the zero depreciation add-on was used. Some insurers limit the number of zero depreciation claims per year (typically 2 to 3) to manage this impact. If you want to protect your NCB, consider adding the NCB protection add-on alongside zero depreciation.

Exclusions and limitations of zero depreciation cover

Engine damage from oil leaks or water ingress is not covered under zero depreciation. A separate engine-protection add-on is required for this.

Mechanical breakdowns and wear and tear are excluded from both comprehensive and zero depreciation coverage.

Claims exceeding the allowed limit (typically 2 to 3 per year) may revert to standard depreciation deductions for subsequent claims.

Vehicle age restriction. Most insurers do not offer zero depreciation for vehicles older than 5 years.

Consumable parts like engine oil, coolant, nuts, and bolts are excluded unless a separate consumables cover is purchased.

Comprehensive vs zero depreciation for two-wheelers

Zero depreciation add-ons are also available for two-wheelers and work the same way as for cars. They are most beneficial for new or premium bikes where replacement parts are expensive. The add-on waives depreciation on replaced parts during claims, reducing the rider’s out-of-pocket expense. The premium increase is proportionally smaller for two-wheelers compared to cars.

When to choose comprehensive insurance without zero depreciation

Your vehicle is more than 5 years old. Zero depreciation may not be available, and the cost-benefit may not justify the premium increase for older vehicles with lower part values.

You have a tight insurance budget. Comprehensive insurance without zero depreciation provides solid coverage at a lower premium.

Your vehicle has low market value. For older cars with low IDV, the depreciation deductions during claims are relatively small in absolute terms.

When to choose zero depreciation cover

Your vehicle is less than 5 years old. The add-on delivers the most value for newer cars, where part replacement costs are high.

You own a luxury or premium vehicle. Expensive body panels, alloy wheels, and headlights attract significant depreciation deductions without zero depreciation cover.

You drive frequently or in high-risk areas. More exposure to accidents means a higher likelihood of needing claims, where depreciation deductions add up quickly.

Conclusion

Comprehensive insurance and zero depreciation cover serve complementary roles. Comprehensive insurance provides the base protection against accidents, theft, fire, and third-party liabilities, while zero depreciation eliminates the depreciation deductions that would otherwise reduce your claim payout. The add-on costs 15% to 30% more in premium but can save significantly more during even a single claim. It is most valuable for vehicles under 5 years old, luxury cars, and high-usage drivers. For older or lower-value vehicles, comprehensive insurance without the add-on may be the more practical choice.

Also Read - What happens to car insurance with no depreciation after 5 years?

FAQs

Q1: Is zero depreciation cover the same as comprehensive insurance?

No, zero depreciation is an optional add-on to comprehensive insurance. Comprehensive is the base policy; zero depreciation removes part depreciation deductions.

Q2: Can I buy zero depreciation cover without comprehensive insurance?

No, zero depreciation is only available as an add-on to an existing comprehensive policy. It cannot be purchased standalone.

Q3: What parts does zero depreciation cover?

It covers most parts, including plastic, rubber, metal, and fibre components, but excludes engine damage from oil leaks or water ingress.

Q4: How does zero depreciation affect my premium?

It increases the premium by approximately 15% to 30%, depending on the vehicle age, model, and insurer's pricing.

Q5: Is zero depreciation cover available for two-wheelers?

Yes, many insurers offer zero-depreciation add-ons for two-wheelers, which are particularly beneficial for new or premium bikes.

Q6: How does zero depreciation impact NCB?

Claims under zero depreciation affect NCB the same way as regular claims. Consider adding NCB protection to preserve your discount.

Q7: What are typical exclusions in zero depreciation cover?

Engine damage from oil or water, mechanical breakdowns, wear and tear, consumables, and claims beyond the annual limit are excluded.

Q8: How does GST apply to zero depreciation cover?

GST at 18% applies to the total premium, including the zero depreciation add-on amount. It is calculated on the combined premium.

Q9: Do all car insurance providers in India offer zero depreciation cover?

Most leading car insurance providers in India offer zero depreciation cover as an add-on to comprehensive policies. However, availability, pricing, and claim limits may vary, so it’s important to compare plans before choosing the right insurer.

Explore more on car insurance

Easy access to more, check out these quick links